Bizum is a service to send money instantly between bank accounts. It was built by banks covering 95% of the market share in Spain. It's currently used by 8 million people, the most used service of this type in Europe. It is a surprising success, which didn't happen elsewhere. This article explains its origin, the reason for its success, how they work to launch new products, and its future challenges.

My interest in Bizum comes from learning different ways of working on a successful product. Bizum has done it, but their way of working isn't standard. They need to align dozens of banks to iterate the product, and the interface, service, and users are controlled by the banks, not by an empowered Bizum product team. They define some guidelines to be implemented by banks. This is the opposite of how I work and what I preach in my articles, which made the conversation very interesting.

All the banks which currently integrate Bizum

All the banks which currently integrate Bizum

How do you align 27 banks?

This is the question that triggered my interest in talking with someone from Bizum. On my job, I have to align people from different countries so we can develop one product which is 95% the same for all. We all work for the same company, and sometimes alignment isn't so easy. What do you do it when you have to align 27 different companies?

"The consultant and the banks decided to organize themselves in working groups to align and make the proposals to the board. They created the legal, business, operational, marketing, and technical working groups. Each group had employees from different banks. Many things had to be coordinated on each of them to launch the product. The board ended up deciding if and how something was done". Fernando shared also that they continue working like that, with ad-hoc working groups depending on the new products they are launching.

What's the Bizum product?

The social object of the company describes well Bizum in fact: "The creation and operation of a common directory in which IBAN numbers of bank accounts are linked to an identifier". The phone number is the identifier.

Simplifying, Bizum is a database of IBAN <> Phone numbers with an authentication platform. Banks are the clients of Bizum, and they are the ones that offer Bizum service to their customers, to all of us. They use the phone number as a proxy to transfer money instantly between bank accounts. If I'm going to send a Bizum from my BBVA account to my friend's account in Santander, BBVA asks Bizum to translate my friend's phone number to his bank account number, and it sends him the instant transfer.

Bizum growth in the last two years

Bizum growth in the last two years

New products

Bank's intention with Bizum has always been to cover all payment use cases. The first idea four years ago was to launch with everything: payment between individuals, e-commerce, and physical payment. However, they made the great decision of going out just with payment between individuals first. They would grow a strong user base, which would serve as a hook for shops.

NGO donations

This was the second use case to be implemented, and it wasn't foreseen at the beginning. Each NGO has a 5-digit Bizum shortcode on which people can donate money. It's working well, Bizum users have donated over one million euros in the last six weeks.

First, they went through the cycle of working groups to align the solution. Then, the board approved the final details. But, to launch and announce the product, each one of the 27 banks had to implement changes in their apps to integrate the new product. That coordination is the challenge and the success of Bizum.

e-Commerce payments

The third use case is more relevant to banks because it allows them to start charging money to merchants since payments to individuals is still free for the end-user.

At this point in the article, it's relevant to remember that the user of Bizum is not their client; he is the client of the bank. The same happens with businesses. The ones who enroll them in Bizum are the banks. That's why the work of banks is vital in the adoption of Bizum as a different revenue stream in online payments.

Some of the merchants who use Bizum

Some of the merchants who use Bizum

Banks have to contact their merchants with virtual POS to activate Bizum on their websites, so their clients can choose to pay with a credit card or Bizum. The more users choose Bizum, the more banks gain traction offering a national payments scheme bringing more competition in the same line as Yves Mersch words.

Future products

Fernando couldn't discuss it. My take here is that Bizum and the banks still have a long way to go, so 80% of e-commerces in Spain accept Bizum. They have a huge opportunity in their hands.

The obvious next step is to go after payments in physical stores or to self-employed people. Businesses already contract the POS with the banks, so that it would be quite a straightforward move. Another attack to cash (80% of all physical payments) and credit cards, and a defensive move towards tech companies. In an article, Fernando comments that they are testing a solution with a dynamic QR code to pay and receive money.

I would suppose Business to Business payments would be the latest use case. It would also be interesting, although the challenge is that businesses in Spain tend to pay at the latest date they can (60 days) or even later. Instant payments isn't a strong value proposition to them.

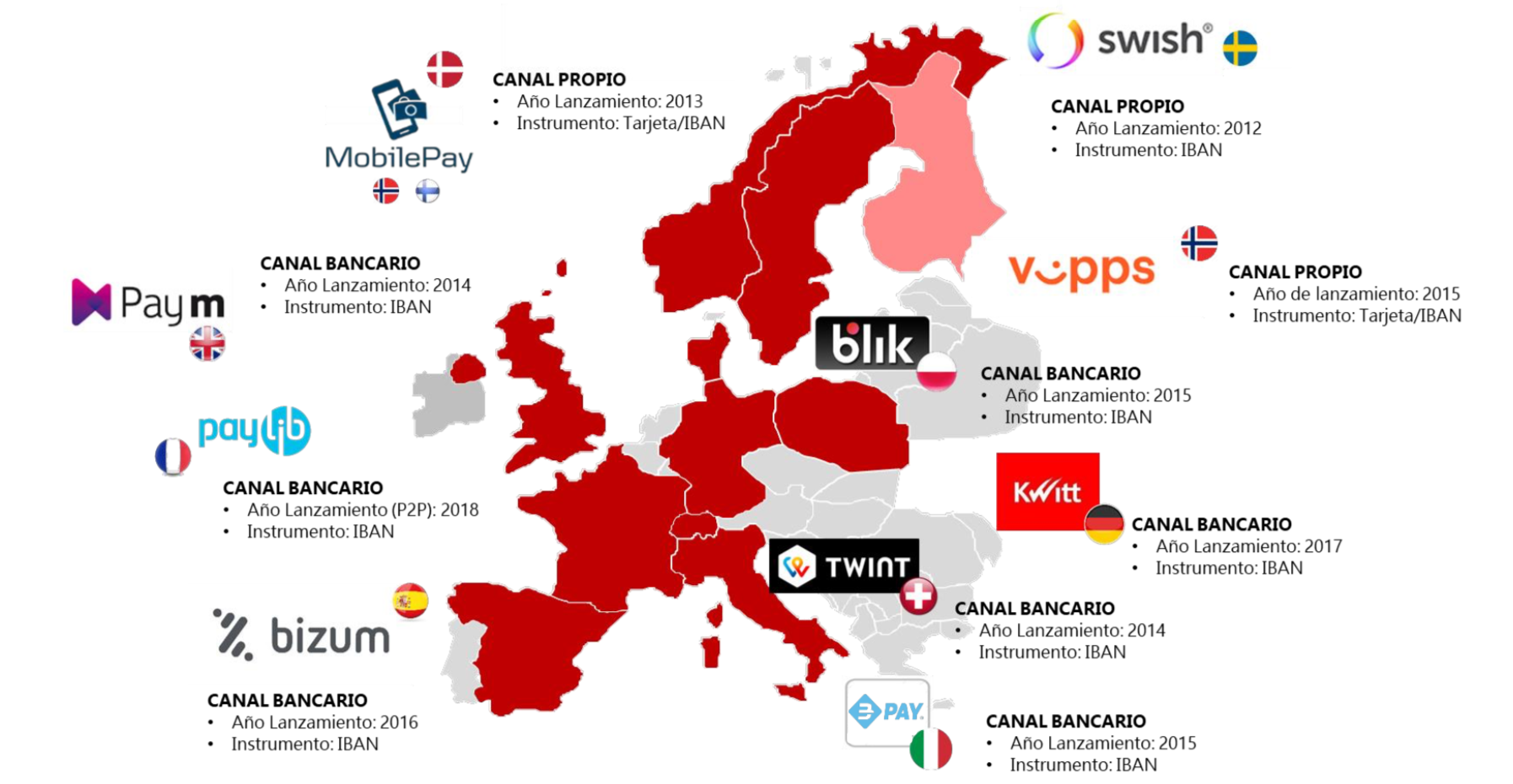

Will Bizum expand to Europe?

Several countries already have services like Bizum. Some of them are MobilePay (Denmark), Swish (Sweden), Vipps (Norway), MB Way (Portugal), Bancomat (Italy), Paylib (France), Pay m (UK), Kwitt (Germany), Twint (Switzerland) and Blik (Poland). However, none of them has the collaboration of all the banks in each country. That's why Bizum is different and has been more successful than their European look-a-likes.

Map of Europe with all Bizum-like services

Map of Europe with all Bizum-like services

Fernando considers this a massive opportunity because "Bizum has the opportunity to be interoperable in Europe. Within this European scheme, why not consider that Bizum can be used as the base? Bizum is highly regarded in Europe. There are countries that could adapt an existent solution rather than creating one of their own. The technological capacity exists; it can be launched in any country."

European banks have the opportunity to build a European solution. Launching Bizum in Europe would help make something truly pan-European interoperable. They have the technology, they have the regulation, they have the users, they have the clients, but will they have the will to work together as the Spanish banks did?

Launching Bizum in Europe would help make something truly pan-European interoperable. If they don't agree on a common solution soon, it's a feasible possibility that Google, Amazon, Facebook, Apple, Stripe, Transferwise, or any other fin-tech start offering instant payments. They can connect to SCT Inst., build their directory of phone numbers/emails to bank accounts, and provide the payment solution to users and businesses. As it's a standard, they don't need to agree on anything with the banks.

This can play out like following the marketplace dynamics of winner takes all. Each solution has its own demand and supply. The one with more users wins. Big tech companies are better at playing that game than banks. So, if they don't move fast, the key to the pan-European payment system could be un-officially controlled by a U.S. company.

My thoughts on their future challenges

Until a year ago, Bizum only had three employees. The rest of the people, especially the engineers, either worked for Redsys or the banks. With that schema, they will reach 12 million users in Spain by the end of 2020.

The main challenge of Bizum employees is to coordinate everyone and inspire, so all banks agree to deliver the product improvements by a specific date. This way of working has allowed them to grow fast because they leveraged the apps and users of the banks. People didn't need to download a new app nor create a new account. This implementation fueled its growth. However, my impression is that it could act now as Damocles' sword.

When any big tech company decides to launch a payment system through SCT Inst., they would have some empowered product teams working on it for the whole of Europe. They can decide on their own; they only need to modify one app; they can launch and iterate fast, looking at data and talking to users.

However, Bizum needs to agree on iterations by consensus, and most banks need to implement the changes or new products before the general announcement can be made. They don't have an app they can improve fast. They don’t have a direct relationship with the user, so every message is channeled through banks. And that's only for Spain. Every Bizum-like app in Europe would need to do the same. That way of working isn't optimized for speed.

Bizum is leading, and that's usually the best time to reinvent yourself. Do the banks want to drive the payments in Europe? Or will they want to play catch-up in a couple of years? My suggestion to them: Make the move, reinvent yourself again.

También puede interesarte

José Pérez-Agüera, Mercadona Tech CPO, on the analytical knowledge and tools Product Managers must know

Mercadona Tech is the tech company from Mercadona, one of the most known supermarkets in Spain. José Pérez-Agüera joined three years ago as CPO. We talked about the analytical skills and tools Product Managers must know and how their relationship with Product Designers should be.

Luisja Alvarez, Telefonica CX, on how their product teams work with multiple countries and brands

Telefonica CX is the department which builds the main consumer app for Telefonica. Luisja is their Head of Global Product since 2018. This article reviews how they structure their product teams to work better with the countries, and how they prepare their quarterly roadmaps.

Ana Asuero, Aplazame CPO, on how to do product when there are limitations you can't control

Aplazame is a Spanish fin-tech company which works with stores to increase their sales using instant financing as a marketing tool. Ana Asuero joined 4 years ago and she is their CPO. We talked about her experience working on the product solving the technical and legal limitations.